Key points:

- Consensus calls: Beat

- Full-year guidance: Raised

- Share price: Lowered

Jean-uine disappointment despite solid figures for the quarter and raised guidance. Traders were uneasy over expansion plans.

👖 A Double Beat, Still a Miss?

- Levi Strauss LEVI delivered better-than-expected quarterly earnings and revenue, then sweetened the story by raising its full-year outlook.

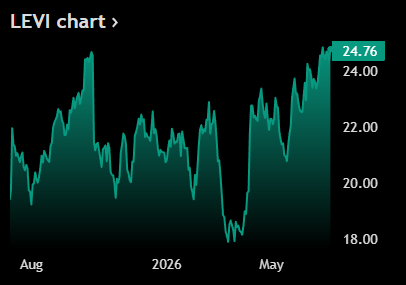

- “It don’t matter,” Wall Street probably, as traders rushed to dump the stock. Shares dropped 6% in after-hours trading after slipping 1.2% during the regular session.

- The denim icon earned 28 cents a share on $1.56 billion in revenue for the quarter ended May 31. Analysts had penciled in 24 cents on $1.52 billion, making it a clean beat on both the top line (revenue) and bottom line (profit).

- Despite the pullback, Levi stock has still climbed more than 25% over the past 12 months, suggesting investors may simply be raising the bar faster than the company can clear it.

🌍 Growth Across the Globe

- Business was strong across regions. Americas sales jumped 9% to $815 million, Europe added 4% to $420 million, and Asia grew 10% to $284 million, with most figures hitting at or above Wall Street expectations.

- Levi also returned $54 million to shareholders through dividends, up 5% from a year ago. Meanwhile, its $200 million share buyback — stock repurchasing to reduce shares outstanding — is expected to wrap up in the third quarter.

- Management raised full-year revenue growth guidance to 7.0%-7.5%, up from a previous forecast of 5.5%-6.5%, signaling confidence that demand is holding up.

🧵 The Market Wants More

- CEO Michelle Gass said Levi’s transformation into a broader denim lifestyle brand continues to gain traction, with women’s apparel sales rising 11% and the company strengthening its market share in both men’s and women’s categories.

- That strategy stretches Levi beyond blue jeans into a wider apparel lineup, digital channels and company-owned stores. The upside is a larger customer base.

- But there’s a tradeoff: Potentially lower prices and tighter profit margins as the company seeks to grab a bigger market share.

- That may explain investors’ hesitation. Wall Street appears less concerned with where Levi is today than with how expensive its next growth chapter might become.

Source: Tradingview

No responses yet