Key points:

- Lucid shares back under $10

- EV maker reports mixed bag

- Loss is wider than expected

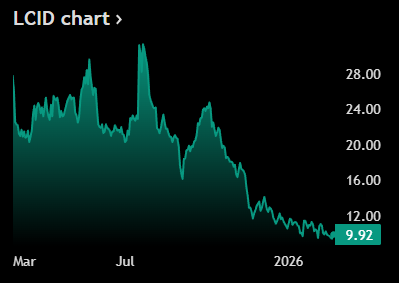

Not-so-fun fact: Lucid shares have erased more than 98% from their all-time peak.

🚗 Revenue Beat, Stock Retreat

- Lucid stock LCID slipped about 5% after the EV maker posted a mixed quarter. Revenue came in at $523 million, well above the $468 million estimate, a respectable beat in a tough EV landscape.

- Earnings were another story. Loss per share widened to $3.62 versus expectations for a $2.62 loss, reminding investors that scale has not yet translated into profitability.

- Markets tend to reward growth with improving margins. Growth with expanding losses? Not so much.

📈 Big Plans, Bigger Hill

- Lucid guided for 2026 vehicle production of 25,000 to 27,000 units, implying growth of roughly 40% to 50% from current levels. Ambitious targets can excite, but they also raise execution pressure.

- The company recently cut 12% of its US salaried workforce, aiming to streamline operations and improve gross margins. Cost discipline is now front and center.

- For context, Lucid generated $1.35 billion in revenue last year, up 68%, yet still posted a $2.7 billion net loss. Scaling remains expensive.

📉 The Long Road Back

- Lucid ended the year with $4.6 billion in liquidity, offering some cushioning. That cash buffer matters in capital-intensive industries like electric vehicles.

- Still, the stock has erased more than 98% from its all-time high. That kind of steep pullback reflects years of dilution, competition, and unmet expectations.

- The outlook is brighter on paper, but investors want proof of sustainable margins and steady production. Until then, rallies may remain short-lived pit stops.

Source: Tradingview

No responses yet