Key points:

- Oracle shares tumble over 10%

- Company to pile more debt

- Big AI buildout = big spending

Software veteran seeks to load up more debt in efforts to cover mounting costs for its AI buildout.

📉 Good Earnings, Bad Reaction

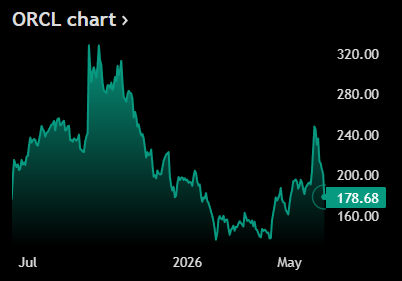

- Oracle delivered a classic Wall Street plot twist: better-than-expected earnings, stronger-than-forecast revenue, and a higher profit outlook — yet shares plunged more than 10% in after-hours trading. Sometimes beating expectations isn’t enough.

- Adjusted earnings came in at $2.11 per share, comfortably above estimates of $1.96 and up from $1.70 a year ago. Revenue climbed 21% year over year to $19.2 billion, narrowly topping forecasts and showcasing continued momentum in Oracle’s cloud business.

- Net income rose to $4.22 billion from $3.43 billion a year earlier. On paper, that’s a solid quarter. On Wall Street, however, the focus quickly shifted from what Oracle earned to what it’s about to spend.

🏗️ AI Buildout Gets Expensive

- Oracle revealed plans for roughly $70 billion in capital expenditures this fiscal year, with customers expected to contribute another $20 billion to $25 billion directly. That’s a staggering jump from the $56 billion spent in fiscal 2026 and $21 billion in fiscal 2025.

- The company also announced plans to raise another $40 billion in fiscal 2027, with the financing expected next calendar year. Investors immediately started doing the math and wondering how much dilution and spending still lies ahead.

- Capital expenditures, or capex, refer to investments in infrastructure such as data centers, servers, and networking equipment. In the AI race, everyone wants bigger computing power. The bill, unfortunately, arrives before the profits do.

☁️ Cloud Demand Still Looks Strong

- Not everything in the report was a cause for concern. Oracle’s cloud engine continues to hum, supported by a massive $638 billion backlog. More than half of that backlog is tied to a single long-term contract with OpenAI.

- The softer spot was guidance. Oracle’s forecast for the current quarter came in slightly below Wall Street expectations, while management left its annual revenue target unchanged at $90 billion despite all the aggressive AI spending.

- The stock had gained just 3% this year through Wednesday’s close, trailing the S&P 500’s 6% advance. Shares also remain down roughly 43% from their September 2025 peak, leaving investors asking whether Oracle is building the future — or simply paying a very high entry fee to get there.

No responses yet