Key points:

- Gold ticks up 0.2% to $4,660

- CPI expected to jump 1% month-over-month

- 45-day ceasefire talks reportedly underway

Both PCE and CPI are set to drop this week. More importantly, perhaps, is what happens in Iran.

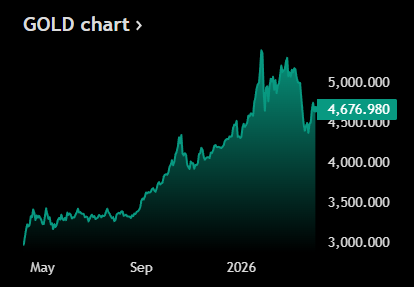

🪙 Gold Holds Steady in a Week Full of Landmines

- Gold XAU/USD edged up 0.2% to $4,660 per ounce Monday morning as traders balanced two competing forces: a potential 45-day ceasefire framework that could remove the war premium from safe haven assets, and a Tuesday deadline from Trump threatening new strikes.

- The Axios report of ceasefire discussions involving the US, Iran, and regional mediators is the most structured diplomatic signal of the entire conflict, but the slim odds of a deal before Tuesday keep gold from pricing a resolution cleanly.

- A confirmed ceasefire would likely send gold lower as the geopolitical fear premium exits. A Tuesday strike on Iranian infrastructure could do the opposite. Gold at $4,660 is the market’s best guess at fair value when both outcomes have meaningful probability.

- Monday is also the first session where markets can react to Friday’s blowout 178,000 March jobs number, which landed on a closed market. A strong workforce reduces rate cut urgency, which raises the opportunity cost of holding gold. The jobs reaction will be part of Monday’s price discovery alongside the Iran deadline and the week’s heavy inflation calendar.

🔥 The First War-Era Inflation Print Arrives Friday

- Friday’s CPI report will be the first inflation reading to capture the actual impact of the Iran war, and the estimates reflect it. Headline CPI is expected to show a 1% month-over-month jump, the largest single-month increase since June 2022.

- The consensus is driven primarily by gasoline prices surpassing $4 a gallon nationally, up more than 35% in five weeks. Year-over-year headline inflation is forecast at 3.4%, which would be the largest annual increase since April 2024.

- For gold specifically, the inflation dynamic cuts both ways. Higher inflation supports gold as a purchasing power hedge, but the Fed’s higher-for-longer response to that inflation raises bond yields and increases the opportunity cost of holding a zero-yield asset.

- The net effect depends on which force dominates, and five weeks of this conflict have shown that the rates channel tends to win over the inflation hedge channel in the short term.

📋 FOMC Minutes and PCE Round Out the Week

- Wednesday brings the release of minutes from the Fed’s mid-March policy meeting, where the FOMC held the federal funds rate steady at 3.5% to 3.75%.

- The minutes will be parsed for any internal debate about whether the war’s inflationary impact changes the rate path, how divided the committee is on the timing of any future cuts, and whether any members raised the possibility of hikes.

- The Bureau of Economic Analysis releases the Personal Consumption Expenditures price index for February on Friday alongside CPI. Economists forecast a 2.8% year-over-year increase, matching January’s reading.

- PCE is the Fed’s preferred inflation gauge and a February print at 2.8% would confirm that even before the war hit, inflation was running above the 2% target with no clean downward trajectory in sight.

- The combination of CPI, PCE, FOMC minutes, and a Tuesday Iran deadline makes this one of the most data-dense and geopolitically loaded weeks of the entire conflict period. Gold sitting quietly at $4,660 on Monday morning is the calm before what is shaping up to be a loud week.

Source: Tradingview

No responses yet